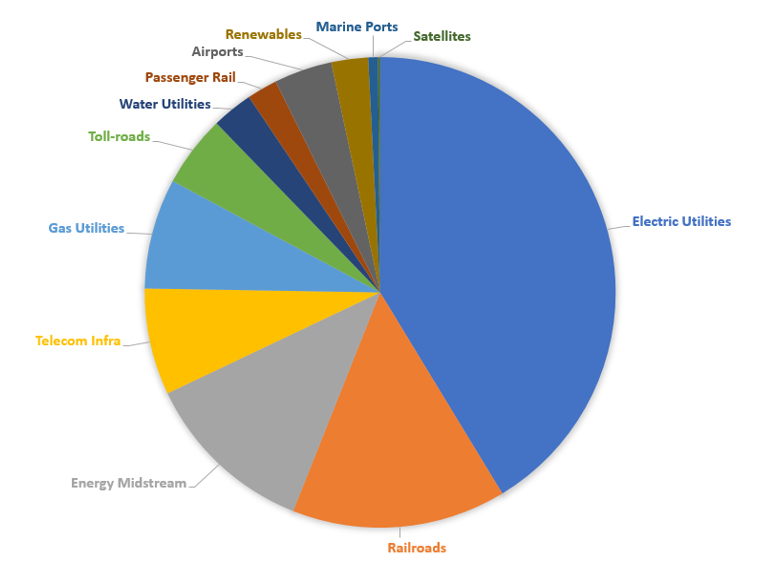

The Infrastructure Asset Class

Many asset allocation models recommend a ~10% weighting to “real assets,” which include infrastructure and real estate. Infrastructure includes power generators, railroads, energy midstream pipelines, data centers, and telecom networks. It also has exposures to gas utilities, toll roads, airports, marine ports, and satellites.

Source: The Global Listed Infrastructure Organization (GLIO)

One often-mentioned positive of the infrastructure asset class is its steadier, contractually supported long-term cash flows—and the yields that can therefore be supported—currently near 4.5%. Cash flows are often further contractually protected from inflation though rising asset values and can be another mechanism of value protection. Another statistical plus for portfolio holdings is the benefits of diversification when adding an asset class of low beta and low correlation with other assets and sectors.

Recent Performance

On the flip side, potential negatives for infrastructure equities can be more short-term volatility because of emerging market exposure, the lumpiness of contract awards, and some limits to perceived growth in an upmarket. A key headwind in the past three years relative to other global indices has been the outsized impact of rising interest rates on longer duration cash flows. Because of this, interest rate debates—further rises, soon-to-be declines, or higher longer?—could impact the space.

Infrastructure Opportunities Ahead

Interest rates aside, there are plenty of potential drivers for infrastructure growth in coming years. One clear driver accelerated to the fore by the Russian war in Ukraine: The trend of moving away from globalization by reshoring material and manufacturing industries. Marine port assets may be impacted, and it takes a while for policy such as the CHIPS Act and then investment spending and associated cash flows to occur. But significant new infrastructure will be required to support growing industrial bases and debottlenecking revised supply chains at home.

Another key driver supporting infrastructure growth should be the many years ahead of work to decarbonize the economy. Many experts suggest $1.5-$2 trillion in annual spending—several times more than what is being spent today—is required to limit temperature change. Global policy steps are gaining momentum. For example, the Inflation Reduction Act has major infrastructure components, and mandatory emissions reporting could motivate lower carbon infrastructure investment.

Power

With electrification being an overriding necessity in a lower-carbon world, significant infrastructure is required in both backbone transmission and local distribution to handle additional and new loads. Much more utility work is being done particularly at the local level in protecting systems from storms, adding capacity to handle developing EV charging loads, supporting energy efficiency efforts, and handling ever increasing digitalization demands.

The power sector in general is also very active in adding renewable generation capacity and battery systems. These all have grid implications and likely some planning complications based on scenarios of when and where adding renewables capacity will be allowed.

Energy midstream

Gas will likely play a part in addressing the growth in global energy needs while also offering a lower carbon emissions alternative to high-carbon emitting energy sources such as coal, wood, and burnt biomass.

Hydrogen and carbon dioxide pipelines should also be an opportunity. LNG liquification and gasification facilities and the pipelines that supply them should continue to be added as imported gas will help a number of countries manage emissions (less coal).

At gas utilities, delivery growth may be challenged by restrictions on new gas hookups in some jurisdictions, but regulated spending should still be encouraged to reduce leaks, add resiliency, add lower-cost monitoring, and improve efficiency where possible.

Transportation

As one of the least carbon-intensive modes of transportation, the railroads remain poised to benefit from the increasing perceived cost of carbon emissions in all supply chains. Marine ports may suffer from the move away from global trade, however ports will also be spending on lower carbon footprints and greater logistical connections with inland distribution centers.

For toll roads, the gradual shift to EVs, which are typically heavier than gasoline powered vehicles and wear roads more, puts added pressure on road maintenance and requires infrastructure spending to accommodate multiple fuel choices for drivers (gas, diesel, electric, hydrogen). In as much as taxes on gasoline go down with fewer gasoline powered vehicles on the road, many jurisdictions may find it necessary to tax on a per-mile or toll basis rather than a per gallon basis. And indeed they may find contracting with professional toll road operators to be a more expedient choice.

Artificial Intelligence and Infrastructure

Because infrastructure assets are long-lived and often take years to put into service, suddenly knowing something faster or more in depth doesn’t necessarily translate into instant change in asset profiles, capacity, or cash flows. Instead, past industry efforts with machine learning and facility optimization should become even more powerful with the application of artificial intelligence and more datasets.

Power

AI computing needs drive significant electricity requirements, but utilities can also use AI to analyze more detailed local usage, make block-by-block outage predictions, generate predictive service requirements, enable faster service response times, and incorporate changing EV charging demands. Incorporating more datasets on winds, sunshine levels, and precipitation into the machine learning analysis should help further optimize last mile service. For gas pipelines and distribution systems, monitoring and reducing carbon emissions and methane leaks and incorporating weather are aspects that pipelines and distribution systems can use AI to improve.

Transportation

Railroads for years have used various data intelligence to optimize their operations through logistics, sensors, car handling, and railcar locations. Further use of AI in considering things such as rail gradients—which impact fuel consumption—is an example of a newer area of interest that can be considered in optimizing train lengths and routing.

On the roadways, in addition to considering gradients in roadway projects, AI can be used to help direct varying flows, accommodate shifting types of vehicles (including autonomous), improve public safety, and optimize demand pricing as traffic levels grow or at least return to pre-Covid norms.

Telecom infrastructure

Data centers and telecom network infrastructure should continue to benefit from growth in the use of AI and rising transmission speeds, which tend to favor systems closer to the user (i.e., more smaller towers and data centers co-located with towers). Digitalization and growing power demand to support digital currencies and artificial intelligence continue to drive the need for more data centers and faster networks (wired, wireless, and satellite).

Conclusion

The changes ahead of reconsidered trade flows, decarbonization, and artificial intelligence should help the infrastructure asset class with future growth and improved operations. There should be a lot of project spending opportunities ahead. That long-term growth should help underpin the asset class even if the economy slows—and particularly if interest rates become supportive again of long-lived cash flow generators.